NowVertical (NOW.V)

An AI turnaround story

Price: CAD 0.35/share (USD 0.2485 using a CAD/USD exchange rate of 0.71)

Market Cap: USD 22.1 million (using my diluted share count)

Enterprise Value: USD 36.5 million

Diluted Shares Outstanding: 88.949 million (see explanation for used share count below)

I wrote large parts of this post before the Q2 results were published, but decided against publishing it due to the very binary outcome. I now believe that with the Q3 results just reported, the risk reward has increased tremendously and the situation has taken on a much less binary feel. I would also note that this is a company that you could easily write a 30 page report on and there would still be some things that you would not have addressed, but I have decided to keep this report short so as not to lose the focus on the simple core of the investment thesis.

“NowVertical Group Inc. is a big data, analytics and VI software and services company that is growing organically and through acquisition. NOW’s VI solutions are organized by industry vertical and are built upon a foundational set of data technologies that fuse, secure, and mobilize data in a transformative and compliant way. The NOW product suite enables the creation of high-value VI solutions that are predictive in nature and drive automation specific to each high-value industry vertical.”

This is how NowVertical describes itself on its website. For a quick overview, I would describe NowVertical as follows:

NowVertical is a failed data analytics consulting roll-up with a short but not very proud history on the Toronto Venture Exchange. The company went public on July 5, 2021 with a closing price of CAD 1.08, since then the share price has fallen in a more or less straight line, brought about by several dilution events that have increased the number of shares outstanding from about 50 million to now 87.1 million (using equity to acquire companies was part of the business model).

The period was also characterized by much turbulence, with many management changes and a dispute with the company's founder and former CEO Daren Trousdell. Trousdell called for the board's resignation in January, stating that the board had led “an incredible erosion in shareholder value” after he stepped down as an officer and director of the company in May 2023. This dispute was eventually resolved in March and Trousdell declared his support for the current leadership team: “I am pleased that the Company and I have resolved our differences and are aligned on a path forward that is focused on creating value for shareholders. I look forward to collaborating productively with Mr. Mendiratta, Ms. Kunda, and the Board in the months ahead.” (https://www.globenewswire.com/news-release/2024/03/21/2850081/0/en/NowVertical-Group-Announces-Resolution-of-Shareholder-Dispute-and-Board-Changes.html)

In addition, the pace of acquisition was far too fast and the approach far too naive, which not only led to a relatively high debt burden for a loss-making company, but also to a lack of focus on realizing synergies. The model, or rather the implementation of the roll-up model, was no longer viable. In particular, the combination of a cash-burning business, a lack of a track record of successful integrations and an already depressed share price (rightly so, of course) would have made additional capital increases massively dilutive, if they had been possible at all, and would possibly have led to a threat to the company's existence in the short term.

Investment thesis

As this is not intended to be a short report, you are probably already aware that my investment thesis is based on a successful turnaround. These are certainly not my favorite situations. Not only because arguably the best investor of all time said that “turnarounds seldom turn”, but also because of my own past experiences as a turnaround consultant.

But here are the things that have already happened and made me believe in a successful turnaround under the leadership of the new management:

New CEO since January, who was previously the seller, founder and CEO of the subsidiary Acrotrend, which had the highest margins in the group in the past

Reduction of the debt burden through the sale of a non-core business (Allegient)

Change of contracts with the current CEO (as seller of the Acrotrend business) to reduce pressure on the balance sheet but also to align his interests with those of shareholders and also reducing the risk of further dilutive capital raises

Changes to other SPAs to better align interests and preserve liquidity

Significant cost reductions to increase profitability

Abandonment of the roll-up model and focus on organic growth as part of an “operations first” model

Integration of the acquired companies and transition to a one-brand-strategy with potentially significant cross-selling potential

Already clearly positive profitability in the latest third quarter results, confirming that the management not only has a turnaround plan, but is also successfully implementing it

Business description

NowVertical is a big data consulting company that also offers some proprietary software products.

As part of its new strategy, the company is changing the monetization model for its software products from simply selling licenses to a more value-added approach by embedding them deeper into its consulting offerings.

The company offers a variety of specialized data solutions for different industries that leverage their industry knowledge to drive key business outcomes. The company calls this vertical intelligence, and the industries it serves are:

financial services

media

technology

retail & e-commerce

subscriptions

The services offered are divided into three categories (gives the customer access to the expertise within the company that is used to provide solutions):

Analytics & Intelligence (Artificial Intelligence, Data Science, Business Analytics)

Data Operations & Engineering (MLOps, DataOps, Data Engineering, Middleware Services

Strategy & Governance (Data Modernization, Expert Assessments, Data Governance)

Offered Solutions are clustered into three categories (using the know how of the company to deliver complex end to end solutions):

Acquisition & Insights (Marketing Attribution, Campaign Analytics, Partner Marketing, Customer Segmentation, Snowgraph)

Engagement & Retention (Cross-Sell and Upsell, Customer Engagement, Customer Retention, Predictive Recommendations, Customer Lifetime Value)

Data Management & Planning (Single Customer View, Single View Reporting, Unified Content Management, Data Risk Mitigation)

Since its foundation, the company has made twelve acquisitions and in the last quarter reported its figures in four segments, namely A10, Acrotrend, CoreBI and Other. In the past, the acquired companies continued to operate as independent companies, which has now changed with the introduction of a single-brand strategy.

The largest segment was Allegient, which was sold in the second quarter of 2024. Allegient's business consisted primarily of staffing services for public sector organizations in the US, and only a small portion of revenue related to data analytics. Profit margins were low and the potential for improvement was limited due to the cost-plus-fee nature of the business. The sale of the business therefore not only relieved pressure on the balance sheet, but also had a significant impact on NowVertical's overall profile.

NowVertical has more than 250 clients, some of which are surprisingly high profile given the size of NowVertical and the way the group has been run in the past. The company states that it has over 30 customers with a customer lifetime value of more than $5 million, and sees significant potential in many other customers that have the same profile but do not yet contribute the same level of revenue. Over 100 of its customers have been identified as strategic customers with an enterprise profile.

Some of their clients are ICBC, Nike, Speedo, Palo Alto Networks, Adobe, Dell, Docusign, Disney, The Economist, Lloyds Banking Group and many others. They have published a lot of case studies on their website that are showing really valuable outcomes for some high profile clients (https://www.nowvertical.com/case-studies).

I find the case study with Adobe particularly interesting, showing how NowVertical worked with them on data analysis for their own marketing campaigns. This is interesting because Adobe has their own software called Adobe Analytics, which is used by many companies to analyze campaign data. They also have a lot of internal consultants who implement this solution and train their clients' employees. I think this is not without a certain irony, but also shows that NowVertical is not a “bullshit” consulting company, but can actually provide real value. (https://www.nowvertical.com/case-studies/adobe)

Financials and valuation

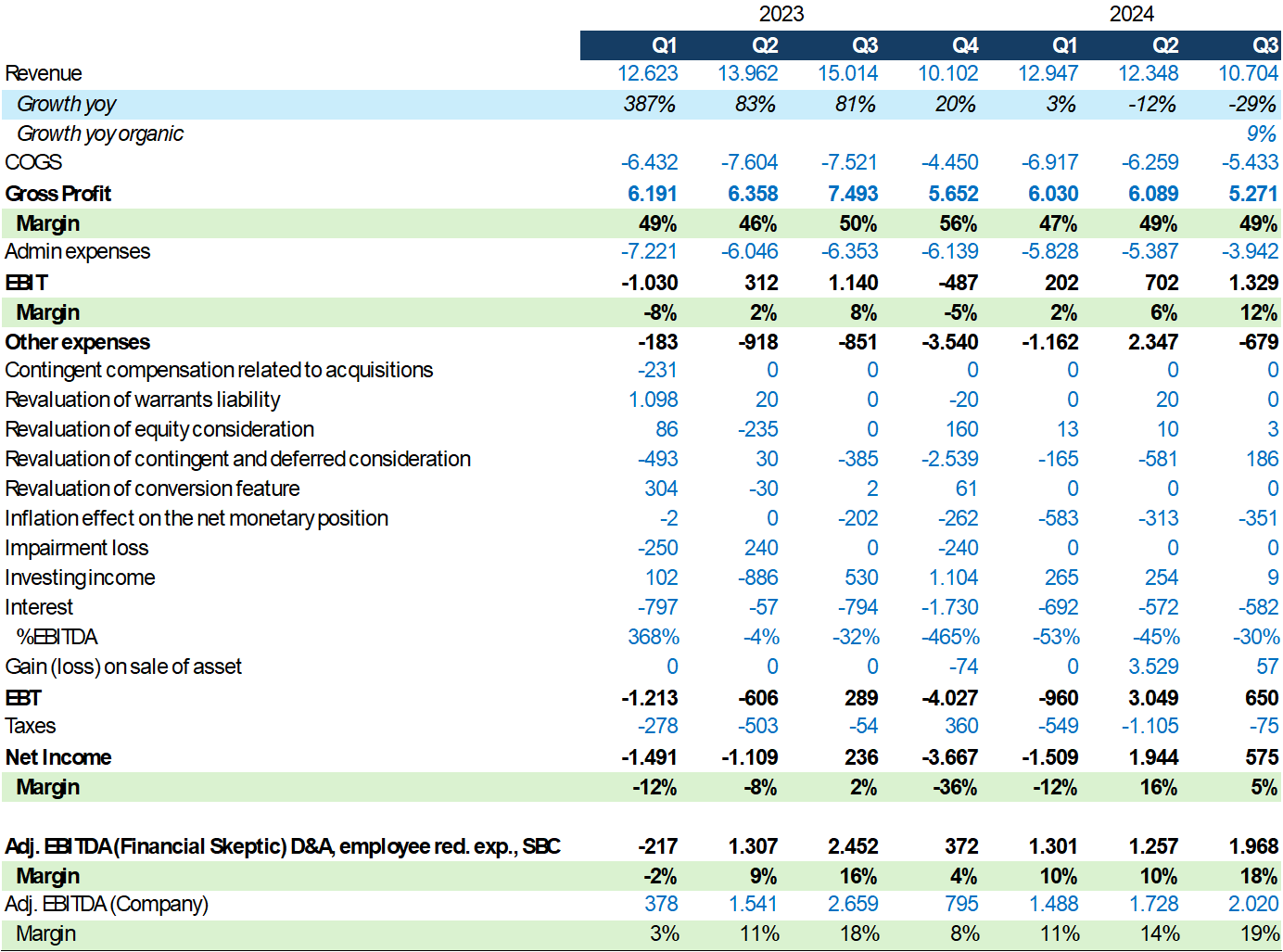

The financial figures for the last few years look pretty awful and often I wouldn't bother to look any further. But in this case, I'm glad I did. The past financials are (imo) not very indicative of the future as they don't give a good impression of the company's profitability potential due to acquisition costs, bloated overheads and unrealized synergies on the cost and revenue side. The combination of non-existent profitability and a balance sheet that does not look very healthy could easily lead to the assumption of imminent bankruptcy.

Fortunately, the balance sheet already looked very different with the Q2 figures, and after the latest Q3 report we have also received confirmation that this company can be run profitably and that the new business model has a lot of potential.

NowVertical has sold the Allegient business for a total of up to 12.5 million dollars, of which the company has already received 7.5 million dollars in cash. Another USD 1 million is guaranteed and will be paid in installments over 18 months after the sale and up to USD 4 million will be paid in the future based on certain revenue milestones. During the Q3 conference call, the CEO stated that the probability of receiving all potential payments related to the sale of Allegient is currently 100%.

Although the balance sheet looks much better now than at the end of the first quarter, the company was not in breach of any covenants at the end of the first quarter prior to these balance sheet improving measures.

Due to the complex capital structure, I would like to explain how I arrived at the share number and enterprise value I used:

The Company has 9,631,500 warrants outstanding with an exercise price of CAD 0.8 and expiring on February 28, 2026, and an additional 3,624,336 warrants outstanding (from the 2022 convertible debt offering) with an exercise price of CAD 1.25, expiring on October 5, 2025. Since these warrants would only be diluted at a much higher share price and the company would also receive significant cash in return, I have decided to ignore them for now as they do not affect the current investment thesis.

The company has 4,378,542 options outstanding at the end of the third quarter. 1,823,333 options have a weighted average strike price of CAD 0.23, 2,250,209 have a weighted average strike price of CAD 0.82 and 305,000 have a weighted average strike price of CAD 1.00. I decided to simplify the investment case a bit by including the 1,823,333 options in a diluted share count, but adjusting the stock-based compensation in my adjusted EBITDA figure. My logic is the same as for not considering warrants.

For similar reasons, I did not include the conversion feature of the convertible debentures in the share count at all, since the conversion price is CAD 1.05. The company has 87.126 million basic shares outstanding, and with the inclusion of the 1.823 million options, I get a diluted share count of 88.949 million.

The convertible note itself is included in the enterprise value (USD 3.276 million), as is the current portion of long-term debt (USD 2.769 million), long-term debt (USD 8.803 million), consideration payable related to businesses acquired (USD 2.335 million), equity and contingent consideration related to acquired businesses that will be paid primarily in cash with a smaller equity component (USD 1.941 million), and long-term consideration related to acquired businesses (USD 2.632 million). However, if you include the consideration to be paid, you should also deduct the outstanding consideration from the sale of Allegient (USD 4 million), to which the CEO said during the last call: “So if you ask us where we stand today, the probability is 100% is one. We will absolutely get that earnout.“

I’m therefore using a debt figure of USD 17.756 million and taking into account the cash of USD 3.324 million, a net debt figure of USD 14.432 million.

The complexity of the income statement is similar to that of the capital structure, and so I am well aware that there is a lot of room for discussion about which valuation metric should be used and what should and should not be adjusted. To arrive at my adjusted EBITDA figure, which is shown here below the income statement, I adjusted the EBIT figure for D&A, expenses related to the workforce reduction and, for the reason I mentioned earlier, stock-based compensation. This gives me an adjusted EBITDA figure of USD 1.968 million for the third quarter of 2024. Annualizing this gives me an adjusted EBITDA of USD 7.872 million and an MC to EBITDA ratio of 2.8 and an EV to EBITDA ratio of 4.6.

(thanks to

who invested a lot of work to build a detailed Excel file from which I am just showing the P&L)A look at the cash flow statement shows a negative free cash flow of USD 0.5 million for the first nine months of the year, but with negative changes in net working capital of almost USD 2.3 million. Free cash flow before changes in net working capital was therefore USD 1.763 million.

Growth potential

NowVertical helps companies leverage AI and other data analysis capabilities to achieve tangible benefits for them in the short term. The company helps businesses capitalize on data they already have but aren't using efficiently, if at all. In other words, unlike many other AI companies, they aren't selling a dream, but rather enabling their customers to use AI in ways that add value today, whether that's in the form of cost savings, revenue increases, or both.

If you have an idea of how you could potentially use AI to improve a process, you can contact NowVertical and they will tell you whether it is feasible and possibly provide you with a solution. Although I am not convinced that AI will change everything in the next few years, I am fairly certain that the use cases for AI and new AI solutions will increase significantly. But that (large) companies are eager to improve their data analytics capabilities is an undeniable trend that has been growing for a few years, and it is not hard to imagine that this is more than a trend given the almost exponential growth of data. NowVertical is far from operating in a saturated market, and the TAM here is not likely to be a risk for growth.

When asked about the company's ability to scale during the last earnings call, the CEO said the following: “So I definitely have a lot of faith and belief in the growth potential of the business going forward and it's almost unlimited growth potential. I can touch upon how we are embedding products into these solutions as well, and that gives us more profitability, and that gets more traction as well in the market.

We are now -- if you look at our revenue size in the U.S., look at our revenue size in the U.K., there's so much headroom just to grow in these markets. Latin America is growing. There are so many emerging markets there. There are so many growth markets, growing economies. You can just keep growing in those markets as well.

I'm not even touching on the inorganic growth potential as yet. That adds another step-up in our growth potential. But that will be on the cards. Once we have proven the consistent organic growth and how we are keeping the margin sustainable, the inorganic growth is going to be a no-brainer. So that's another level of growth we will bring about.

So I would say, unlimited growth potential in the business. We can keep working on this for 10 years, and we will not have a single dull day.”

In my opinion, they do indeed have a very interesting geographic presence. They have two delivery centers in very interesting geographies, namely Argentina and India, which not only offer relatively cheap labor but also enable NowVertical to provide services worldwide 24/7. In addition, after selling Allegient, they generate over 70% of their revenue in Latin America and some of the remaining revenue in the Middle East, giving them an already strong position in rapidly growing markets. I think this is a good starting position to grow in North America as well. Many of their large customers are US companies anyway and they also have very interesting strategic partnerships in Latin America with technology companies, i.e. the large cloud providers. In addition, they also have a relatively good market position in the UK due to the business that the new CEO sold to the company (Acrotrend).

I believe there is a great deal of potential to increase revenues just by selling services and solutions to existing customers, but the one-brand strategy should also lead to a much more powerful company that is likely to be perceived quite differently by its seemingly already satisfied customers in the future. Some customers would probably not entertain the idea of asking their LATAM service provider to also provide services for the core US market, but it is probably a completely different story if you believe that you are not working with a small Colombian company, but instead with a global company that is listed in North America.

There should also be many easy wins when it comes to realizing synergies. Due to the new one-brand strategy, the company is bundling the competencies of all subsidiaries for the first time. During the conference call on the third-quarter results, the CEO already mentioned an example of a contract win based on the bundling of already existing competencies:

“One of the case studies or incidents that I could share with you is in a large media and entertainment client, we have now been able to sell one of the contracts on the financial forecasting modeling in the tune of $750,000. This is again, by bringing various capabilities together from the business. Otherwise, we would not have been able to position ourselves within that high-value contract in just one contract, if you like, because we didn't have enough capabilities in one part of the business.

And this particular contract has been actually won against one of the incumbent Big 4s, and we have replaced that incumbent Big 4, which was a big deal, I would say. So these are some of the examples that I just wanted to bring in. There are more, but we are getting traction. We are seeing traction, and our clients are appreciating the combined strength of the business as well in our solutions and services.”

Conclusion

We see a company here that seems to be undergoing a very impressive turnaround. But, in my opinion, that is only the beginning and not the end of the story. I don't see a company that is getting back on track for the first time and where everyone is satisfied with steady small profitability. In my opinion, we are looking at a company with a lot of growth potential that has been poorly managed and has the potential to work its way up from a former bankruptcy candidate to a successful turnaround and finally to a very good growth story. In my opinion, this kind of potential is usually not trading at a EV to EBITDA multiple of 4.6 for long.

Disclaimer: The sole purpose of this report is to explain the rational behind the investment I made on my own behalf. This report reflects an opinion and is for informational and entertainment purposes only. It is not intended as investment advice. It may contain errors, and I may change my opinion expressed in this report at any time. You should always do your own due diligence and never blindly follow anyone in an investment. I as well as the company I control and members of my family hold this stock in personal accounts.

This stock is also part of the portfolio of the wikifolio FinancialSkeptic Value, which I manage and which is mirrored by an investable (probably only for Germans, Austrians and Swiss) certificate. You can find more information about my Wikifolio with this link (German).

I really appreciate what kind of nonsense companies (in a positive way) you dig up. It always goes from „what is this?“ to „Ah, I get it“ and even though they would not be in my considerations (for the most part), I enjoy getting those thoughts.

Thanks for the write-up – I think its an interesting opportunity to explore. I have scanned the financial statements quickly to get a high level view. What is your take on the following two topics:

1) Net Working Capital consuming Cash in the past 21 months

The working capital of the business seems to structurally consume cash. In FY 2023, it consumed USD 4m. YTD P9 2024, it consumed USD 2,2m. Assuming an annualized EBITDA run rate of USD 8m, it feels as if the NWC is going to eat significant chunks if the potential FCF, if NWC keeps consuming so much cash.

In addition, YTD P9 2024 NWC increase is driven by an increase of roughly USD 2.9m of unbilled revenues recognized on the balance sheet. Do you have any clue about what is happening here? This could be a single large project that they are working on. On the other hand, it wouldn’t be the first business that is trying to fool investors with posting fake revenues and profits.

2) Potential seasonality influcing the improvement in EBITDA margin

The Adjusted EBITDA margin in Q3 2024 was 19%. Compared to Q2, Q1 and Q4 it shows a strong improvement. However, compared to Q3 2024, the EBITDA margin is just 1% higher as the margin back in Q3 last year was 18%. To what extent are the improvements real improvements versus driven by potential seasonality?