Radcom Ltd.

Will a shadow from the past become a light for the future?

Price: USD 12.00/share

Market Cap: USD 204 million (using the diluted share count)

Enterprise Value: USD 94 million

Diluted Shares Outstanding: 17 million

RADCOM Ltd. is a software company that provides telecommunications operators and communication service providers (CSPs) with 5G-enabled, cloud-native solutions for network intelligence and service assurance.

It was the first company I researched when I became a full-time investor. That was over six years ago, and it seemed like an investment that didn’t require much thought. To me, it looked like one of the best companies ever, and there was a chance that its total addressable market (TAM) would grow exponentially due to the upcoming rollout of 5G networks, which require sophisticated service assurance solutions—and Radcom had the most innovative and forward-looking solution on the market. I even remember telling someone, in perfect Dunning-Kruger style, that I really wouldn’t know what I was doing if this weren’t a great investment. I bought the shares for about $9 apiece, and today they’re trading at $12.00. Assuming I had held onto my original shares until today, I wouldn’t be particularly thrilled with my return over the past six years.

Although the rollout of 5G—and 5G Standalone in particular—is proceeding much more slowly than I had originally expected, I wasn’t too far off the mark regarding the business itself, and I still consider it an absolutely fantastic business. Where I was very much mistaken, however, is in how the company is using the enormous cash reserves on its balance sheet. I thought they would do something meaningful with it or return a large portion of it to shareholders once they had achieved consistent positive cash flow and profits.

They spent $2.5 million on what appeared to be a great acquisition (Continual Ltd.) that enhanced their product offering, but aside from that, they simply chose to pile even more cash onto the balance sheet, which now totals $110 million.

Investment thesis

The reason I believe this is a good investment right now can be summed up quite simply: I expect that there will be significant changes in capital allocation in the future, or even a sale of the entire company, which should result in a significantly higher valuation multiple than the market is currently willing to grant.

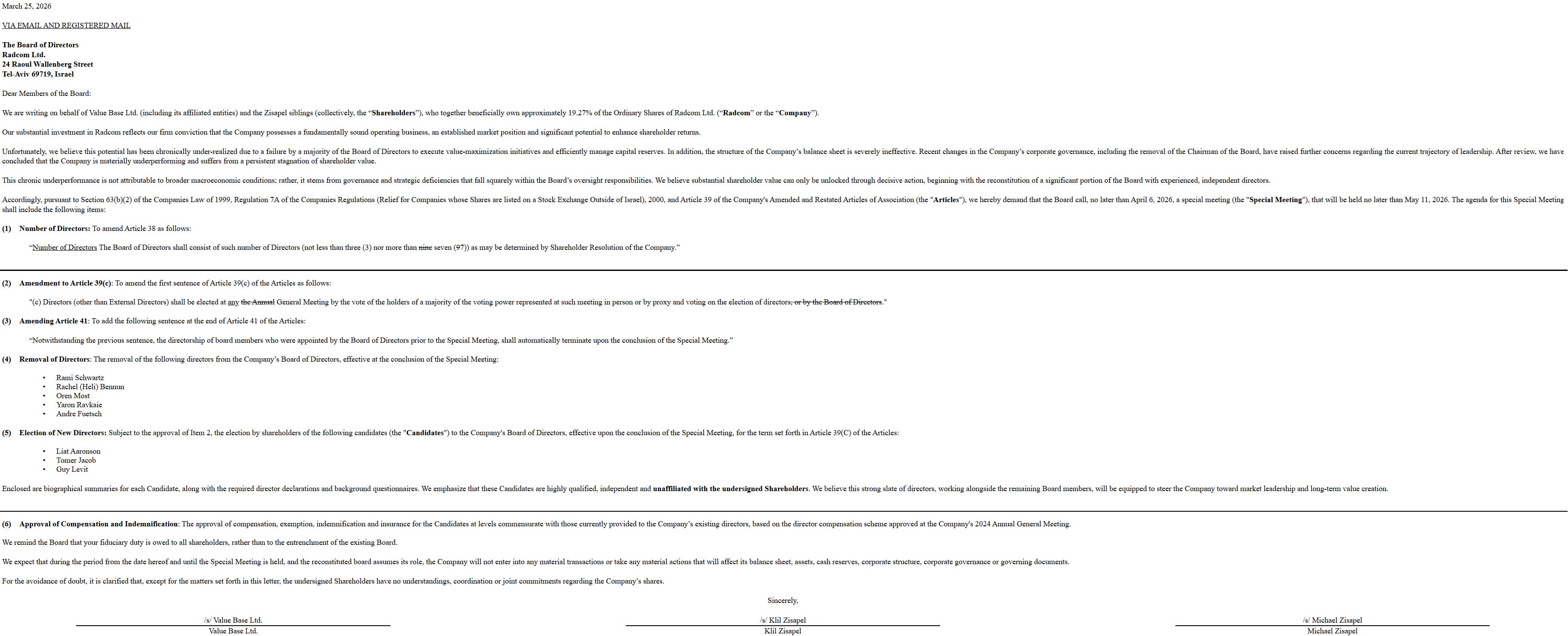

On Febraury 17th Value Base Ltd. filed a 13D. This alone probably does not justify the conclusion that a change is highly likely, since Value Base holds only slightly more than 5% of the company and there are far larger shareholders, such as the Zisapel siblings (children of founder Zohar Zisapel) and Lynrock Capital, which is the largest shareholder. The Zisapel siblings have also filed a 13D form in the past, but there were no signs that they were pushing for significant changes; therefore, the 13D/A filing from February 24 is not a strong indicator of an actual change.

However, one day later, on February 25, Lynrock Capital not only filed a 19.3% ownership report—which is a significantly higher stake than the 14.9% reported at year-end, as stated in a 13G form a week earlier—but also amended its 13G filing to a 13D form and added the following sentence:

“The Reporting Persons intend to engage in communications with the Issuer’s board of directors (the “Board”) and management team regarding opportunities to enhance shareholder value. The Reporting Persons believe that the Issuer should commence a process to evaluate strategic alternatives to maximize shareholder value. The Reporting Persons intend to discuss their views with respect to the foregoing matters with the Issuer, its shareholders, and other market participants.”

A week later, on March 26, the Zisapel siblings and Value Base filed 13D filings in which they stated that they were part of a group, and sent the following letter to the board of director:

Given Lynrock’s efforts to explore strategic alternatives, I consider it highly likely that they will vote in line with the activist group at the extraordinary general meeting, which would secure approximately 38.6% of all votes and thus ensure that the Group’s proposals are almost certainly approved.

For those who are not yet familiar with the company, the next question is likely to be about its current valuation and the quality of its business. I will explain the business in more detail below, but in summary, I still believe this is one of the best businesses. Due to the nature of the software business, the company has very high operating leverage; due to the nature of the solution itself, which is business-critical, it has very high customer loyalty; and, combined with the nature of Radcom’s customers—which are telecommunications companies—it has a business that is highly recession-resistant.

If you’re concerned about AI, I can tell you that I view progress in this space as a very positive development for Radcom, as the company has the best and most comprehensive dataset, brings the most experience to the table, and uses AI wherever it makes sense to help its customers realize the vision of an automated communications network made possible by Radcom’s solution.

You are getting this company at an FCF-to-MC ratio of 13.4, based on a cash flow of $15.2 million in 2025. Excluding net cash and the resulting investment income, the company is trading at an EBIT-to-EV ratio of 11.3, based on an operating profit of $8.3 million in 2025. Even with moderate growth in 2026, the multiples will be significantly lower at year-end due to the extremely high operating leverage.

I consider this a highly asymmetric opportunity, where your downside risk is somewhat hedged by a low valuation and your upside potential is very high, as Radcom’s value to a potential strategic buyer is likely to be significantly higher than its current market capitalization.

Business description

There are almost endless aspects of the company that could be discussed, but I don’t consider them particularly relevant to this specific investment opportunity, so I’ll simply try to provide a brief overview of the offered solutions.

The company is operating in the service assurance space. Its solutions ensure that services offered over networks meet a pre-defined service quality level for an optimal subscriber experience.

It is therefore easy to see why a fservice assurance solution is of great importance to a network operator and represents a business-critical component at the core of its operations.

Radcom offers cloud-native, 5G-enabled, and fully virtualized service assurance solutions that enable telecommunications operators to gain end-to-end network visibility and insights into the customer experience across all networks; RADCOM Network Visibility, a cloud-native network packet broker and filtering solution that enables CSPs to manage network traffic at scale across multiple cloud environments and control the level of visibility to perform analytics on selected data sets; and RADCOM Network Insights, a business intelligence solution that provides insights for a wide range of use cases, enabled by data captured and correlated via RADCOM Network Visibility and RADCOM Service Assurance.

In addition, the company offers solutions for mobile and fixed-line networks, including 5G, LTE, Voice over LTE, Voice over Wi-Fi, IP Multimedia Subsystem, Voice over IP, and Universal Mobile Telecommunication Service. The company sells its products both directly and through a network of independent distributors and resellers in North America, Asia, Latin America, Israel, and worldwide.

The services provided by Radcom’s products are required by every telecommunications network operator and are essential for a high-performance next-generation network. The solutions monitor the network, making the network and the processes occurring within it visible to the operator. They are capable of quickly resolving network performance issues to ensure the delivery of high-quality services in mobile and fixed networks. They provide insights and automated root cause analysis powered by artificial intelligence (AI).

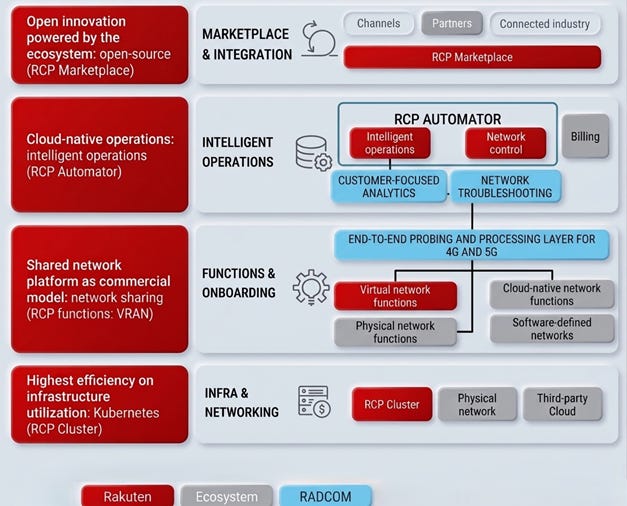

The picture illustrates Radcom’s role in Rakuten’s network architecture. Radcom’s solutions are indispensable to the network operator. They serve as the link between the physical network and cloud operations. They provide the data needed for intelligent operations and handle network troubleshooting. As a result, these solutions form the core of next-generation (virtualized) networks.

Two recent major innovations that demonstrate Radcom’s technological leadership in its field are Radcom Neura and Radcom High-Capacity User Analytics (HCUA).

“RADCOM Neura is our agentic AI framework that leverages trusted, customer-centric data from RADCOM ACE and a comprehensive set of AI/ML tools to power a team of customer experience and service assurance AI agents. It integrates seamlessly with service management and OSS/BSS systems, helping operators improve operational efficiency and elevate customer satisfaction by building a customer-aware, intent-based network. RADCOM Neura AI agents operate autonomously to transform assurance data into a unified source of truth, linking network operations with customer-focused teams. By automating case validation, service quality analysis, root-cause analytics, and customer experience improvements, Neura helps operators deliver better service, increase customer satisfaction, boost efficiency, improve first-call resolution, and lower ticket volume.”

HCUA is based on the NVIDIA BlueField-3 DPU and provides real-time analytics at a fraction of the cost. Radcom claims to be the first provider to capture 400 Gbps on a single server, resulting in operating costs up to 75% lower than those of traditional probes and offering complete network visibility. The product is currently undergoing lab and field testing with key customers and is gaining strong momentum. While the company has not commented on this, the ability to monitor every user behavior on the network could pave the way for an entry into the business analytics sector with a TAM similar to the service assurance business (my speculation).

Radcom was honored in the “Best AI/ML Innovation” category at the 2025 Global Connectivity Awards. The company’s solutions are ready for deployment on all major hyperscaler platforms, and Radcom has partnerships with AWS, Google Cloud, and Microsoft Azure. Last year the company also announced a partnership with Servicenow “to offer advanced automated complaint resolution. The new solution provides ticket validation and prioritization to significantly reduce the time and effort network engineers spend on investigating and resolving technical issues and complaints.”

Financial figures and valuation

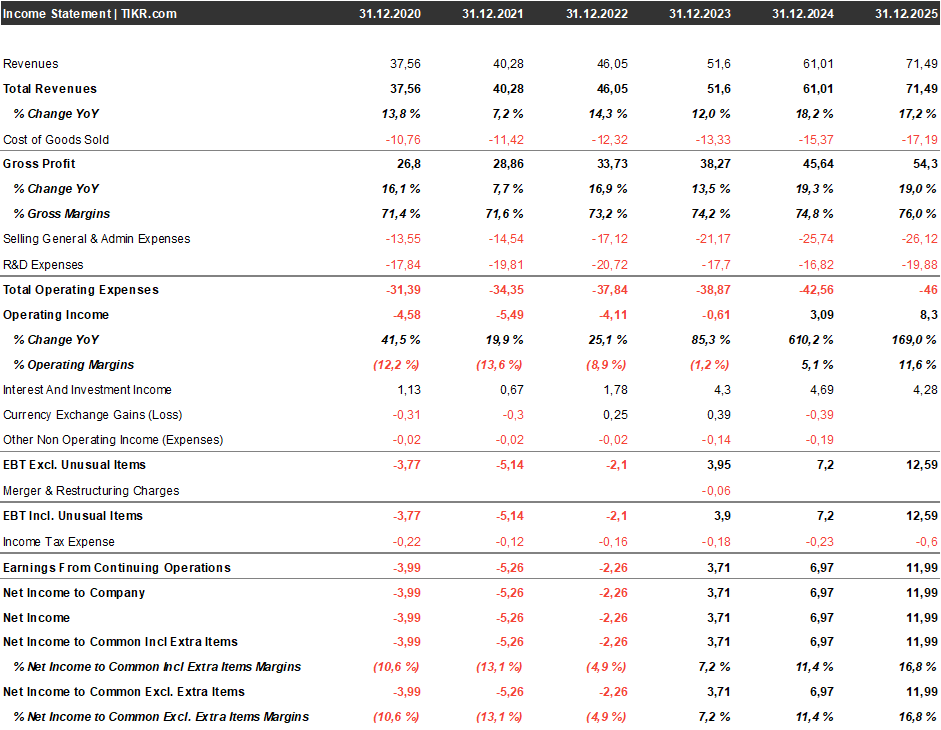

While a look at the financial figures doesn’t necessarily point to “hypergrowth,” it undoubtedly shows steady progress. And given the extremely high operating leverage, steady progress is probably all that’s needed.

source: Tikr

Incremental gross margins are around 80%, and research and development costs—including the most recent innovations—are fully expensed, which makes the current profitability appear to be a very conservative projection for the future.

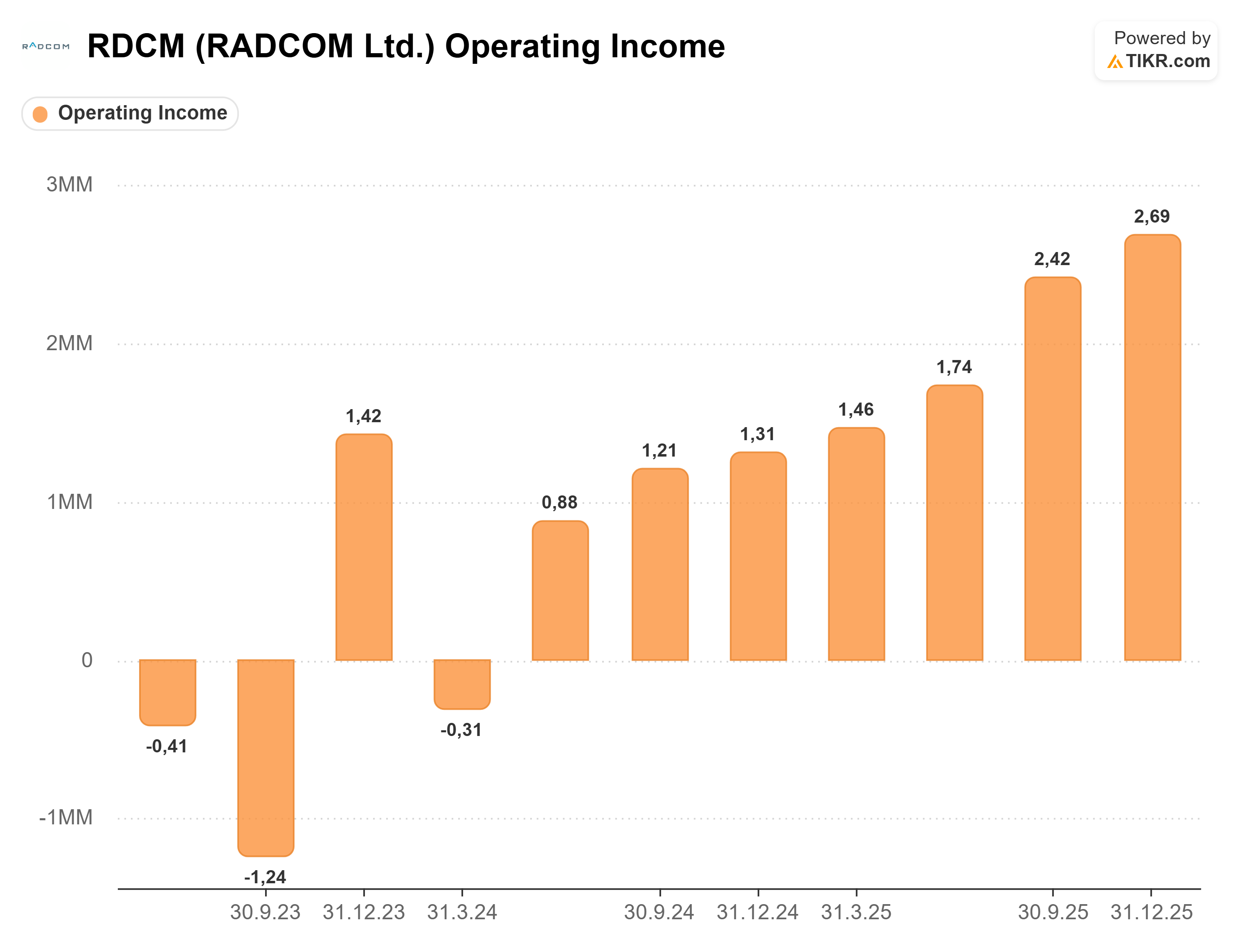

A look at the quarterly results makes this even clearer. The last quarter was the seventh consecutive quarter to show profit growth compared to the previous quarter.

Let’s do a quick calculation: The company closed out 2025 with an annualized operating profit of $10.8 million; for this year, it expects (based on the midpoint of a revenue growth forecast of 8–12%) revenue growth of $7.1 million, which, at an incremental margin of 80%, would result in an additional gross profit of $5.7 million. Assuming they increase selling, general, and administrative expenses (SG&A) and R&D expenditures by $3 million compared to the annualized fourth quarter, we arrive at an additional operating income of $2.7 million and a total operating income for 2026 of approximately $13.5 million, along with a year-end run rate that is significantly higher.

This would mean that, based on realistic expectations for 2026, the stock would trade at an EBIT-to-EV ratio of 7 or an EBIT-to-market capitalization ratio of 15.1, with approximately $130 million in cash at the end of 2026.

Risks

The company has a very high concentration of customers: in 2025, 86% of revenue will come from three customers. This is partly due to the business model and because the first customer for Radcom’s software-based solutions was AT&T itself, the largest customer that can be acquired in this sector. In addition, the customer Rakuten Symphony essentially acts as an intermediary and encompasses several end customers. Nevertheless, there is a risk that the loss of a single customer could lead to a significant loss of revenue.

The Board of Directors consists of 9 members, and overall stock-based compensation has exceeded $6 million in each of the past two years, which I believe is a substantial amount. Combined with a steadily growing, unused cash balance, this does not exactly demonstrate shareholder friendliness, and should the activist fail to succeed, this will likely continue to weigh on the stock price and somewhat overshadow operational progress.

Conclusion

I view this as a highly asymmetric situation in which it is likely that we will see a catalyst in the near future that unlocks significant shareholder value; however, even if this catalyst fails to materialize, there is still a high probability of a good return based on a moderate valuation combined with steady fundamental improvements. I am reluctant to provide price targets or model hypothetical upside potential, but I think many would agree that a buyer can be found for this company willing to pay 20 times operating income. With operating income of $13.5 million and cash reserves of $130 million at year-end, this would correspond to a share price twice as high as today’s. Everyone should do their own calculations, but I do not consider this example to be overly optimistic.

Disclaimer: The sole purpose of this report is to explain the rational behind the investment I made on my own behalf. This report reflects an opinion and is for informational and entertainment purposes only. It is not intended as investment advice. It may contain errors, and I may change my opinion expressed in this report at any time. You should always do your own due diligence and never blindly follow anyone in an investment. I as well as the company I control and members of my family hold this stock in personal accounts.

This stock is also part of the portfolio of the wikifolio FinancialSkeptic Value, which I manage and which is mirrored by an investable (probably only for Germans, Austrians and Swiss) certificate. You can find more information about my Wikifolio with this link (German).