Tier1 Technology S.A.

A company with a hidden software asset that not too many people seem to care about

A few days ago Isaac published a write-up about my current largest position and I thought why not follow up with a short post. You’ll find Isaacs write-up here:

TIER1 Technology S.A. (TR1.MC)

Price: €2.42/share

Market Cap: €24.2 million (including 239,100 treasury shares as of June 2023)

Enterprise Value: €20.4 million

Shares Outstanding: 10.0 million

Overview

Tier1 Technology is a Spanish IT services and software company focused on the retail sector (66% of sales in 2023) and in particular on food retail.

The company has a very interesting and, in my opinion, not well understood or recognized strategy. This coupled with a recent jump in profitability that is not yet priced into the stock makes it an interesting investment case in my opinion. The core of my thesis and the main driver of profitability is the transformation from a mainly IT services focused business with a relatively low margin profile and fluctuating results to a software dominated business with a very high margin profile and more consistent results. The company offers a few different software products but the crown jewel and driver of profitability is the on unified commerce focused retail software comerzzia.

The company had a five-year strategic plan that expired at the end of 2023. The core of the strategic plan was to grow through acquisitions, focus on the retail sector and grow the key software product comerzzia. Unlike many other companies that announce fancy plans, they delivered on every point, and in terms of inorganic growth, they didn't just do something stupid to be able to say they did it, instead it seems like they have made clever small and cheap acquisitions that all had a specific benefit besides additional revenue.

The company held a presentation on January 23 where it also gave a preview of the figures for the 2023 financial year. It reported revenue growth of 19% to € 21.8 million and a 68% increase in EBITDA to € 3.2 million. The market reaction to this announcement was small and very short-lived, which shows how little attention this company is receiving. That Looking at the share price chart, one might assume that the company has stagnated since its listing in 2018. My personal opinion is that they have got their priorities right and instead of promoting their stock, they have achieved a lot of things in these years that are not obvious to "superficial market observers". Moreover, they financed everything they did from cash flow, did not dilute and even paid a regular dividend.

Tier1 currently has a market capitalization of around €24.2m (including some treasury shares) and a net cash position of €3.8m (according to the company presentation at the end of FY23), resulting in an EV of €20.4m and an EV/EBITDA ratio of 6.4. It is very likely that comerzzia's growth will continue at double-digit rates for the foreseeable future, leading to a steady increase in margins. The broader market does not even seem aware of the 2023 numbers already achieved, let alone understand the transformation and potential of this company.

Structure of the group

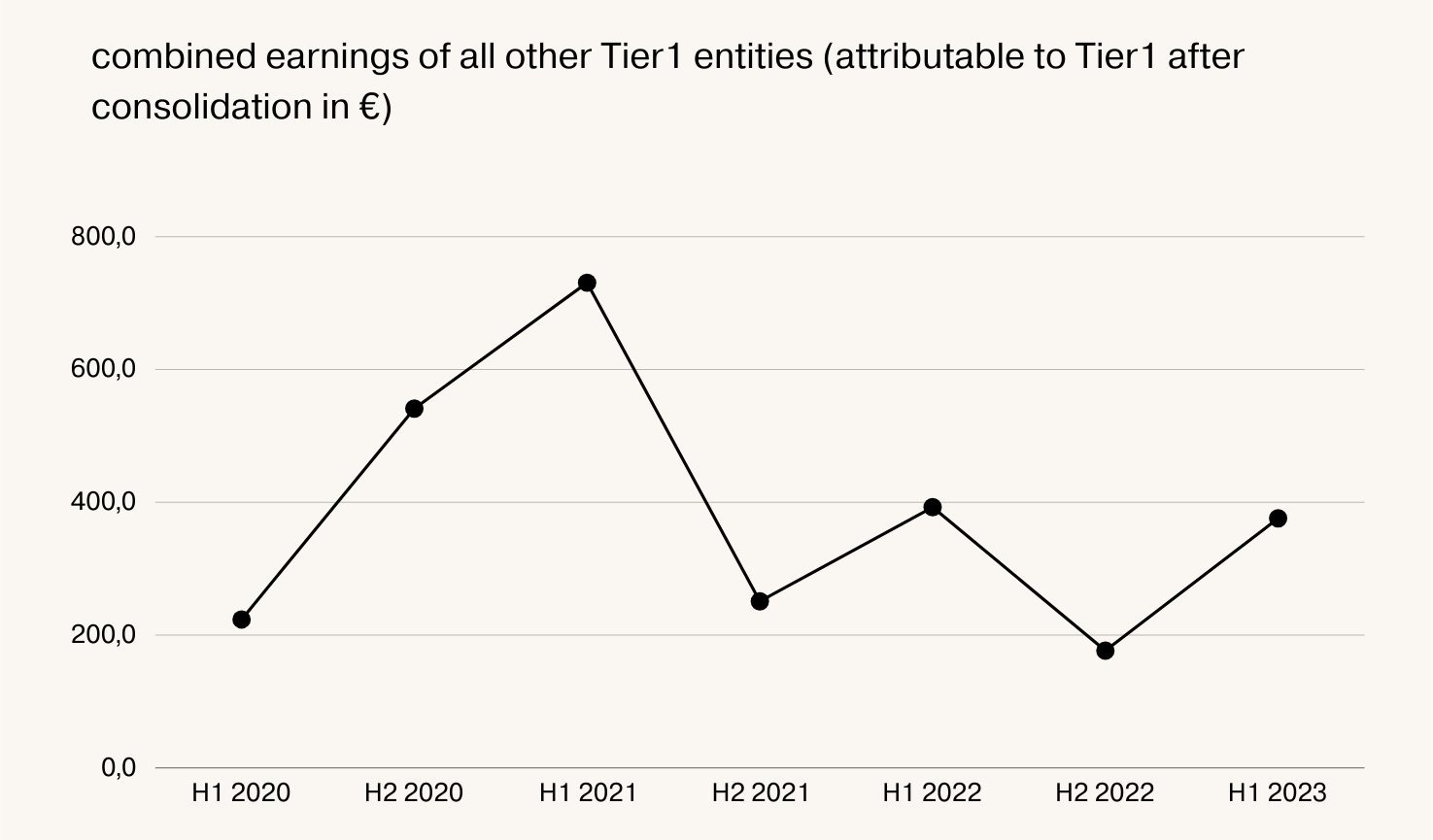

Tier1 reports in two segments, "Infrastructure" (IT services and other activities) and "Software Products". On the infrastructure side, the company provides IT infrastructure deployment and maintenance, contract software development, software implementation and maintenance, and some business process outsourcing services. My understanding is that this happens in the operational Tier1 business, Tier7 and Dinamic Area (see picture below, red background). About 2/3 of the revenue from software products comes from comerzzia and its subsidiaries (blue background), while the main product (comerzzia) resides in the comerzzia subsidiary, which is 90% Tier1 owned. The other 1/3 of software revenue comes from various products that are not specifically tailored to retail companies. To get an idea of how profitable the operating companies are and therefore an idea of which company and therefore which solution the revenues are derived from, I have added the consolidated half-year results for the period ended June 30, 2023 of the individual companies (profit share of the Tier1 group after minority interest, intercompany eliminations, overhead allocation and other consolidation effects). The investment in nextt was only added in the second half of FY23, was therefore not part of the report and will only be included in the FY23 report using the equity method due to the minority interest. Only recently (February 2024) Tier1 exercised a call option to acquire a further 12% of the company, so that Tier1 now owns 52% of nextt and it is therefore consolidated from the current period's report. In financial year 23, nextt generated revenue of € 1.7 million, consisting of 100% recurring revenue, and broke even at EBITDA level.

In the following, I will concentrate on the software side, as this is the strategic focus of the company and this is where the opportunities lie.

Software solutions

Comerzzia is the company's main software asset and was responsible for a majority of software sales in FY23. Comerzzia was from the beginning developed with a unified commerce focus in mind. The software is very modular and offers a wide range of capabilities as confirmed again and again by gartner. As part of the comerzzia software family they are separately offering comerzzia Enterprise Suite POS (software that enables the core activities of a retailer with a focus on unified commerce, starting at 89€ per POS and month), comerzzia Enterprise Suite Involve CRM Loyalty (loyalty and marketing solution that measures the impact of different campaigns and promotions in an online store and a loyalty app to improve proximity with the customer that is able to establish the loyalty plan of the retailer, starting at 250€ per month and user), Comerzzia Online Store (online store solution with functionalities for Food and Non-Food retailers, the online store functions as another store, with unification of prices, promotions and customers, and complete visibility of the inventory in order to offer consistent experiences through the different channels) and comerzzia Involve CRM Analytics (advanced analytics module that provides you with in-depth knowledge about customers, allows to personalize the sales and communication strategy to offer a unique experience and differential value, starting from 2600€ per month and user). Comerzzia solutions are offered as 100% SaaS cloud solutions as well as a 100% on-premise installations. They have standard integrations in the most important ERP solutions (like SAP, Oracle and Microsoft) as well as in other sector relevant solutions (Adyen, Paypal, Shopify, Magento and so on). Additionally, they are proud of their open architecture and even give their clients access to their source code to make every thinkable integration possible. I think this is a meaningful differentiator from many of their competitors. They are also advertising the solution with the claim to have the lowest total cost of ownership in the industry.

Atractor is a “standard modular and scalable business management solution that can be configured and adapted to the different functional areas of the company for any sector of private activity or public companies. Optional modules: Accounting/Financial, Purchasing/Sales/Warehouse and Project Management.” The solution is part of the operational Tier1 company and pricing starts at 400€/month. They are also offering some additional modules for Atractor, for instance a b2b web store solution.

ELEVATORWARE is a “standard modular and scalable business management solution for elevator operators that can be configured and adapted to the different functional areas of the company for any sector of private activity or public companies. Modules: maintenance, Installation or rehabilitation and Economic-financial.”

SecurInvoice is a platform that automates the Immediate supply of VAT information (SII) in an agile and secure manner, guaranteeing the exchange of information and compliance with the standard of the electronic headquarters of the Tax Agency. Electronic billing solutions designed to integrate with the clients own information systems. Sending invoices compatible to and according to Spanish regulations.

Nextt is a comprehensive software solution for restaurants and the latest acquisition. The software suit offers among other things POS-software, kitchen software, a backoffice module, an e-commerce and delivery module and business analytic solutions.

At first glance, I dismissed the relevance of all solutions besides comerzzia. But after doing a little research, I found out not only that these solutions currently account for around 1/3 of software product sales, but also that there is at least some optionality hidden in these solutions.

Elevatorware, for example, should have cross-selling potential within the current customer base and could perhaps also offer surprise potential if, for example, they can convince an elevator manufacturer to resell their solution. SecurInvoice might offer a more concrete opportunity. The Spanish government is in the process of introducing the "Crea y Crece" law. Part of this law is mandatory electronic invoicing for B2B transactions. The law is likely to be introduced in the next few months, after which companies with a turnover of more than €8 million will be given 12 months and companies with a turnover of less than €8 million will be given 36 months to introduce e-invoicing capabilities.

All in all, I don't think you need to see growth in the ex-comerzzia solutions to make the investment worthwhile, but I am confident that we can at least expect similar revenues from these solutions in the future, and it's nice to know that there is at least a chance of positive surprises.

The following charts show that the earnings growth comes from comerzzia.

During the last year comerzzia entities were for the first time responsible for the majority of Tier1’s earnings while their earnings were sequentially growing 233,9% in H1 2023 from H2 2022, indicating very strong operational leverage.

In their last presentation Tier1 presented a figure for order intake. Incoming orders for software products amounted to €7.8 million in 2023, an increase of 48% compared to the previous year. This lets me think that anything other than double-digit growth in software revenue for FY24 would be a big surprise.

Internationalization

Following the successful implementation of its 5-year strategic plan, Tier1 announced that one of the company's main focuses going forward will be internationalization. Although the company's solutions are used in over 60 countries, internationalization has not really been pushed forward so far. In fact, there was not even a dedicated team or even person responsible for internationalization. Existing international users are often Spanish companies that also use Tier1 solutions at their international locations. This will change this year and Tier1 will set up its own internationalization team.

However, some steps have already been taken with partners. In Brazil, a 50/50 joint venture has been established with Seidor S.A. to develop the local market. Seidor is a large and fast-growing IT consulting company (turnover of 836 million dollars in 2022), which is a 10% co-owner of comerzzia and an implementation partner. It's certainly not your typical nanocap partner. The 50% stake in the Brazilian subsidiary as well as the 10% direct stake in comerzzia also seems like a good incentive. Tier1 has already stated that they are willing to duplicate the joint venture model in other LATAM markets.

A second very interesting partnership was announced last December with Retex in Italy. Retex is also a consulting company, but with a clear focus on retail and a special emphasis on unified commerce. They are now an implementation partner for comerzzia and I suspect that they will not offer many different omnichannel solutions for their clients to choose from, but will recommend one that is able to turn their omnichannel recommendations into reality. Retex has a turnover of around €100 million and has many tier one customers such as coop, crai, Lavazza, Starbucks, Armani and many more. Javier Rubio commented on the partnership as follows: "This alliance will allow comerzzia to deploy its solution in a significant number of points of sale in Italy, a country with around 28,865 supermarkets and grocery stores." (translated from the Spanish original)

A little bit surprising, in a positive way, was an announcement comerzzia made this week. The company partnered with Inteum and they are now an implementation partner for comerzzia. Inteum has over 2.5 billion Euros in revenue, 28.000 employees and operates in 27 countries. Although it seems the partnership is predominantly focused on the Spanish market for now, this is also a big opportunity to drive international growth. I am very impressed with the speed at which Comerzzia is entering into potentially very significant partnerships and it is hard to imagine that Comerzzia's growth rates will slow down in the short to medium term. I consider these partnerships also a confirmation of the strength of the solution as multibillion dollar companies in general don’t tend to enter into partnerships with very small companies unless they see a big potential.

These are things that have already happened recently, before the internationalization team has even started its work. I am pretty confident that they can be very successful with their internationalization, and since they are using local implementation partners, they really have nothing to lose and a lot to gain.

Conclusion

Tier1 is a company that trades at an EV/EBITDA ratio of 6.4. The company likely has a lot of software growth ahead and the margin of incremental revenue should be very high, a combination that makes the valuation look very undemanding. In the short term, I see great potential for upside once the market recognizes the company's operating leverage and comerzzia’s growth potential. In the medium term, I expect further improvements in fundamentals based on the contracts already won and the internationalization initiatives. If they remain very disciplined, this could be a much bigger and much more successful company in the future.

Please be aware that what I have written here about is only a fraction of the information I looked at before deciding to invest in the company and I also do not know if I will follow up with further posts about the company.

Disclaimer: The sole purpose of this report is to explain the rational behind the investment I made on my own behalf. This report reflects an opinion and is for informational and entertainment purposes only. It is not intended as investment advice. It may contain errors, and I may change my opinion expressed in this report at any time. You should always do your own due diligence and never blindly follow anyone in an investment. I as well as members of my family hold this stock in personal accounts.

Unfortunately, due to the limited investing universe at wikifolio, it is not part of the portfolio of the wikifolio FinancialSkeptic Value, which I manage and which is mirrored by an investable (probably only for Germans, Austrians and Swiss) certificate. You can find more information about my Wikifolio with this link (German).

Hi, thanks for the write-up. What value does Comerzzia provide that other pos and crm giants do not? Just trying to understand how defendable this software is in their niche from larger competitors. thx

Hello, I did not accept the tender offer from Retex, so my small position in Tier1 is now blocked in my broker, I would like to ask you what can I do with them now. Thank you in advance and hope you can clear those doubts